If you’ve inherited an IRA from a parent or another loved one, it is likely that you have an Inherited IRA (aka, Beneficiary IRA). These can be powerful accounts, but you need to understand the Required Minimum Distribution (“RMD”) rules for your Inherited IRA to properly utilize it. The inherited IRA may be a Traditional or Roth IRA, and there are three different distribution options you may elect when you inherit the IRA. These distribution options dictate how you can invest in the account. Please note that if you inherit an account from a spouse, you can just do a spousal rollover and consider the account as yours. This article is for those inheriting an IRA from a non-spouse.

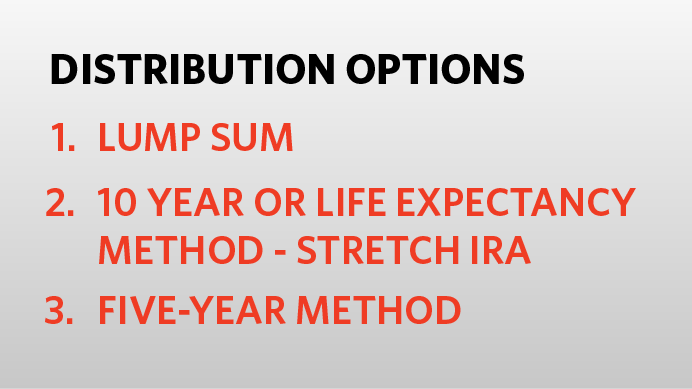

Distribution Options

You will have three distribution options upon the death of your loved one to receive the funds from their IRA. In general, the best option is the “Life Expectancy Method” as it allows you to delay the withdrawal of funds from the IRA, and allows the money invested to grow tax-deferred (Traditional) or tax-free (Roth). The three options are outlined fully below:

1. Lump Sum

The first option is to simply take a lump-sum and be taxed on the full distribution. There is no 10% early withdrawal penalty (regardless of your age or the deceased owner), but you are taxed on the amount distributed if it is a Traditional IRA. You’re also giving up the tax-deferred (Traditional) or tax-free (Roth) benefits of the account. Don’t take this option. It’s the worst tax and financial option available to you.

2. 10 Year or Life Expectancy Method – Stretch IRA

Important update to this method under the SECURE Act signed into law in 2019. Those who have already inherited an IRA in 2019 or earlier can still operate as usual. Everyone else who looked forward to one will have to take solace in the fact that they at least have 10 years of “stretching” to continue investing the funds in a tax-free (Roth) or tax-deferred (Traditional) manner. And, under the new rule, there is no RMD rule in effect each year. Instead, the total amount must be distributed at the end of 10 years. This makes things a little easier with self-directed assets and also helps any IRA owner – 10 years is still a good amount of time – get a little bit of additional tax-deferred (Traditional) or tax-free (Roth) growth.

For those that inherited an IRA in 2019 or earlier the following option is still available, whereby you can take distributions from the inherited IRA over your lifetime based on the value of the account. These distributions are required for Traditional IRAs and even for inherited Roth IRAs. For example, if you inherited a $100,000 IRA at age 50, you would have to take about $3,000 a year as a required minimum distribution each year and the rest can stay invested. The RMD amount changes each year as you age and as the account value grows or decreases. There is no 10% early withdrawal penalty when you pull money out of the account regardless of your age. Traditional Inherited IRA distributions are taxable to the Beneficiary while Roth IRA distributions are tax-free. And yes, Inherited Roth IRAs are subject to RMD even though there is no RMD for regular Roth IRAs.

3. Five-Year Method

This option is available to all inherited Roth accounts but is only available to inherited Traditional IRAs where the deceased account owner was under age 72 at the date of their death. Under this option, the Inherited IRA is not subject to RMD. However, it must be fully distributed by December 31st of the fifth year following the year of the account owner’s death. There is no 10% early withdrawal penalty, and distributions are subject to tax. Again, this option is only available to Traditional accounts.

Investing with a Self-Directed Inherited IRA

Stretching out the benefits of an inherited IRA can be powerful, but make sure you plan for RMDs before you make any self-directed investments from your Inherited IRA.

Self-directed Inherited IRA accounts can be set-up in as little as five minutes here at Directed IRA.